The era of managing employer-sponsored healthcare costs through plan design changes and cost-shifting is over. Middle market employers are facing a runaway cost curve that threatens the economics of their business. Over the past decade, employer-sponsored health coverage costs have surged nearly 50%, far outpacing both wage growth and inflation. Today, the average health plan costs employers nearly $17,000 per employee per year. (i)

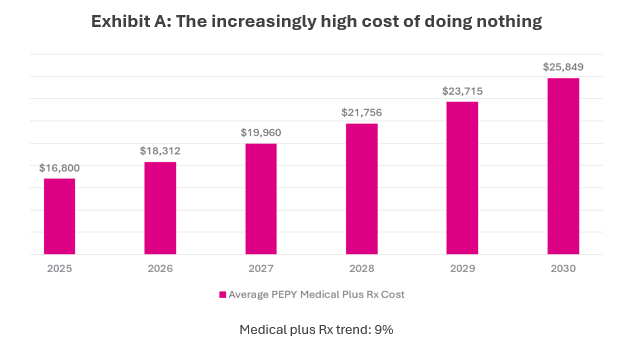

The pressure is accelerating. Overall employers now face the steepest benefit cost increase in 15 years, with costs projected to climb 9% in this 2026 plan year alone.(ii) Middle market employers are experiencing much higher increases. If nothing changes, the average plan will top $25,000 per employee by 2030. (See Exhibit A.) For a middle market company with 1,000 employees, that equates to about $25 million in annual healthcare spending, rivaling payroll as the largest business expense.

Middle market companies are defined here as companies with 100-3,500 employees

The Cost Drivers for Healthcare are systemic, but several have gained momentum:

- Rising pharmacy costs. Prescription drugs account for 30% of total healthcare spending, growing 13–15% annually.(iii) Specialty drugs comprise half of total drug spending and will continue to rise. (iv)

- ACA and Medicare changes. Loss of premium subsidies could leave 3.8 – 4.8M people uninsured (v), shifting costs to employer-sponsored plans and driving premiums.

- Worsening physician shortages. Gaps in emergency medicine, primary care, psychiatry, and rural care are intensifying due to new visa restrictions and limits on international medical graduates, adding further cost pressure.

“Putting aside tariffs and the cost of capital – two things we can’t control – the alarming cost and business risk of healthcare has quickly become the must-address topic in our boardroom.”

CEO, Manufacturing – 620 employees

Stark realities for employees

Over the past decade, payroll contributions, deductibles and out-of-pocket maximums have climbed steadily, quietly eroding real take-home pay even as wages rose nominally.

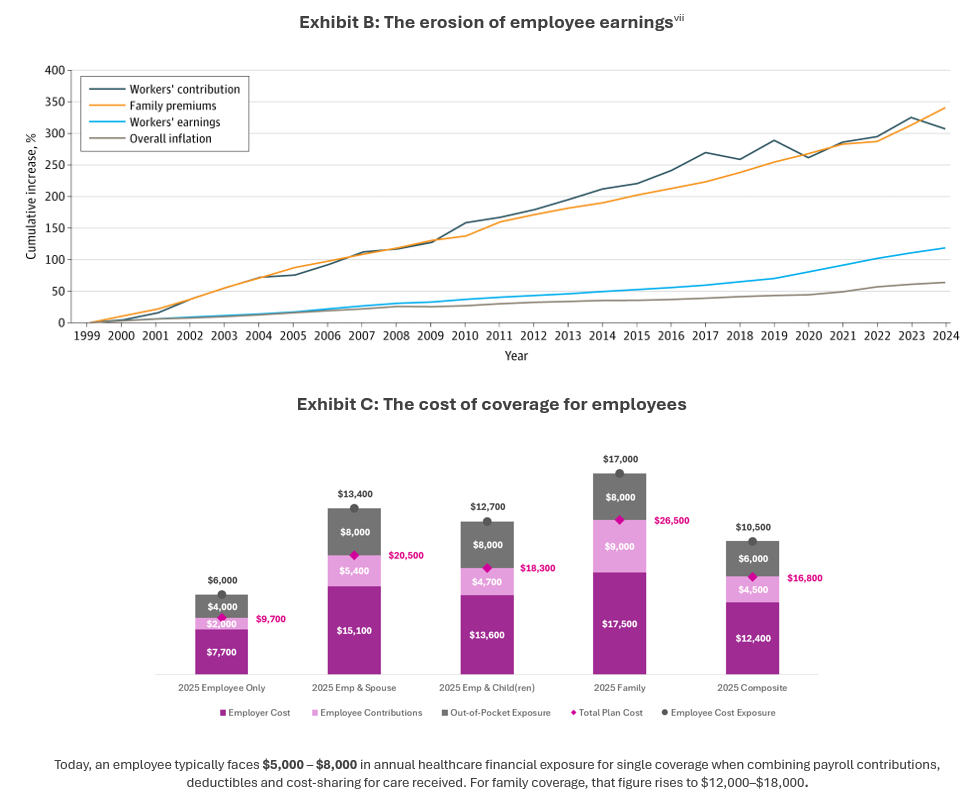

The data tells a clear story: for more than two decades, healthcare costs have outrun both wages and inflation, and workers have been losing ground ever since. (See Exhibit B.) The result is a healthcare system that increasingly prices people out of their own care: Thirty-six percent of adults now report avoiding or postponing treatment because of cost.(vi) (See Exhibit C.)

Yet despite its impact on both employers and employees, healthcare remains among the least strategically managed risk in most middle market organizations – a troubling reality given its scale and trajectory. “Business as usual” is not sustainable. If current trends hold, rising healthcare costs will increasingly squeeze employers out of their investment in wages, talent and growth, and compound financial pressure on employees in the process. (See Exhibit C.)

Leaders of middle market companies who fail to address this risk today are allowing the persistent threat of accelerating healthcare costs to undermine both the financial health of their organizations and the wellbeing of their workforces.

Middle market companies can borrow from the approach that large and jumbo organizations already use – treating healthcare as a strategic financial risk and partnering with brokers (including consultants) to apply the same governance, analytics and long-term planning they bring to every other major operating expense. But, while middle market companies are too complex for standardized solutions, they’re often considered too small by many brokers to dedicate the necessary resources they give their largest clients.

The opportunity — and the imperative — is to close that gap between what middle market employers need and what brokers traditionally offer them. Because when benefits are managed with the same discipline and financial rigor applied to M&A or any other major cost center, the outcomes speak for themselves: better results for employees and more sustainable costs for the employers who fund their care.

Helping middle market employers build and deliver appropriate solutions to manage healthcare risk

The healthcare landscape is shaped by countless stakeholders. Yet for middle market organizations managing health plans, two key stakeholders can meaningfully change the trajectory for your costs and risk, and you have the power to change their behaviors: employees and brokers.

Employees (“Decision-maker/Consumer”) are at the heart of any sustainable, consumer-driven healthcare model. When people are equipped to make informed, high-value decisions about their care, costs become more predictable and, ultimately, more manageable. Most employees want exactly that: 91% say they would choose the lowest-cost (and quality) option if pricing were available upfront, but only a small percentage feel equipped to do so.(viii)

Brokers (“Advisors/Partners”) are subject matter experts there to help you identify and manage risk and assess plan performance throughout the year. But with most brokers, there is a fundamental misalignment: in most cases, their compensation isn’t tied to outcomes – in fact, it’s often tied to total healthcare spending. They are simply not held accountable for bringing down the magnitude of spending on healthcare. Their energy tends to be concentrated in the four or five months when next year’s plan design is on the table, leaving the other seven or eight months underserved and without a long-term plan.

It’s the employer’s job to define what’s expected of both the employee and the broker and make sure those expectations are met throughout the year. That begins with defining clear responsibilities, aligning incentives and offering the right tools for decision-making.

“The healthcare system is impossible to navigate. It is very, very difficult to understand how to find quality doctors and compare costs.”

Fintech employee

It also means having the right team in place – people who can work with the broker and your internal finance team to create a funding arrangement that lets the organization realize the impact of better employee health decisions. Whether the plan is level-funded, self-insured or captive-based, the funding model should drive active cost management and long-term accountability, not simply redistribute costs from one year to the next. Your risk management strategy must move in lockstep with that model to prevent unintended financial exposure. This shifts benefits from a transactional HR function into a governed financial and strategic priority and may call for new capabilities within your team.

How to Change Your Healthcare Plan Trend: Steps for a Governance Playbook

Healthcare plan cost management isn’t achieved through cost-shifting or isolated plan changes. It’s achieved when employers take responsibility for actively influencing brokers and employees. Employers are the change drivers and “System Designers.” Period.

Employers who follow this Playbook – taking control where they can, holding brokers accountable and purposefully reinforcing/influencing the right employee behaviors – will drive meaningful change in their healthcare trend.

PLAYBOOK

Priorities for “System Designer:” Employer establishes internal goals and accountabilities to set direction

- Dedicate a senior finance resource for forecasting, monitoring and predictive modeling performance year-round

- Assess funding options every one-to-three years as a risk management strategy decision – your risk profile changes regularly

- Simplify choices – offer two meaningfully different medical plans and make information easy to access

- Adopt plan designs and network strategies that steer members to higher-value care through financial incentives

- Provide decision support tools to help employees identify high value care based on cost and quality

- Make plan design and vendor decisions based on total cost of care, not networks or fees alone

- Pursue utilization-based compensation point solutions in place of per-employee-per-month (PEPM) fees

- Provide healthcare navigation and advocacy support to guide members through complex care decisions

- Communicate the “why” to employees – this is what’s driving the upcoming plan changes

- Eliminate passive enrollment

- Maintain strong plan hygiene: dependent eligibility and claim audits

- Communicate year-round, not just during open enrollment

- Treat vendor oversight as a core fiduciary responsibility

- Hold brokers accountable for their responsibilities

“I’ve been fighting for years to have ‘a seat at the table’ with my peers in leadership.

This year, I lost all credibility with our 19% healthcare renewal.”

Vice President, Human Resources, publicly-held services company, 1,800 employees

PLAYBOOK

Priorities for “Advisors/Partners:” Employer establishes new or expanded responsibilities for brokers

In high-performing organizations, the broker is far more than a renewal manager or benefits middleman. The broker is a strategist, operator, commercial steward and performance leader, actively helping employers manage population health risk and control healthcare spending.

This demands a fundamental shift: from transactional brokerage to continuous plan management, and from broker to trusted advisor. The broker to a middle market company should:

- Offer a transparent broker compensation structure, whether through commission or fee-based structure

- Place fees at risk against service level guarantees

- Provide documented, executable multi-year strategy to align HR/finance/leadership

- Provide data, modeling and strategic guidance to help leadership make an informed funding decision that aligns with cost and risk management goals (i.e., self-insured, level-funded, captive, self-funded)

- Recommend solutions that actively steer employees toward higher-value care

- Build rewards-based strategy for consumer behavior – real choices and real rewards

- Conduct market reviews and hold vendors accountable for performance

- Renegotiate and audit PBM contracts every two-to-three years

- Conduct quarterly performance reviews to assess, course correct, communicate

- Maintain a structured compliance audit process and ongoing compliance calendar

- Make account team accessible and focused on planning, performance, employer/employee issue resolution

“Self-insurance only works when the organization is prepared to actively manage it. Without the right structure, data, and discipline, it becomes a funding change, not a strategy.”

Elliot Rosenblum, President, Symphony Consulting

“Employers need to pay close attention and analyze the demographics of their workforce – each additional year of average employee age increases total plan cost by roughly 2–3%. Negative economic factors are compelling employees to stay longer in their jobs, and AI is hollowing a swath of entry- level jobs – typically younger workers. This will compound and have a material impact on costs and trend increases, especially mid- to longer-term.”

John Ryan, Senior Advisor, Symphony Consulting

PLAYBOOK

Priorities for “Decision-Maker:” Employer creates path to move employees toward educated healthcare consumers

Employee decisions directly shape healthcare costs and outcomes. While the plans their employer offers set boundaries of their choices, employees still have meaningful agency in influencing what those plans cost. Employers – often in partnership with their brokers – need to create communication, tools and resources that enable employees to:

- Treat open enrollment as one of the most important financial and health care decisions for their family – not an administrative hassle

- Recognize that cost and quality are often not aligned – the most expensive care or best-known providers are not always better

- Use decision-support tools to make informed decisions on care including choosing the right care option (e.g., physical therapy before select surgery) and selecting higher-quality, lower-cost providers

- Understanding coverage and cost before receiving care

- Actively engage in benefits education opportunities – materials, meetings, etc.

- Provide feedback to benefit/HR/finance leaders on plan usability and communication

- Share experiences with colleagues on decision support tools and solutions

“It baffles me how little attention people pay to their healthcare costs. Most employees spend more time comparative shopping for headphones than understanding their fourth biggest yearly expense right behind housing, food and transportation.”

CFO, $450m privately-held hospitality company

The opportunity for middle market employers to take control of healthcare costs has never been more urgent

Middle market employers who are willing to take accountability and manage their healthcare plans differently can implement practical, proven solutions by aligning stakeholders and incentives, using data to inform decisions and designing benefits that balance financial realities with human needs.

“We incurred a crushing 22% increase in healthcare costs this year, net of plan design changes and cost-shifting to employees. I need a trusted advisor who can help me put in place an executable, precise strategy to break this cycle.”

CFO, $300m consumer products

Realizing these opportunities calls for a mission-critical focus and new mindset toward the broker relationship, funding arrangements, plan designs, your HR model and employee engagement.

Employers who act now and demand accountability from themselves, their brokers and their employees will do more than control costs. They’ll improve health outcomes and build a meaningful strategic advantage over competitors still relying on the same approaches that created today’s challenges in the first place.

The organizations that act now will regain control. Those that don’t will be defined by the consequences.

Communication: A Necessary Investment

Employee behavior doesn’t change in a vacuum — it changes when employers actively give people the tools, context and confidence to make better decisions. That requires communication and it requires commitment.

Effective, year-round communication builds trust, drives adoption and closes the gap between strategy and behavior. It is not a support function — it is a core component of a high-performing healthcare strategy. Yet for many middle market employers, it remains chronically underinvested, even though middle market employers have distinct advantage over larger companies since they can more easily and directly access their employees.

Underinvesting time and resources into communication is a costly oversight. Behavior change only happens when people have the motivation, the information and the means to act differently. Employers who treat communication as an afterthought are leaving one of the most powerful levers in cost management largely untouched.(ix)

References

i https://www.kff.org/health-costs/2025-employer-health-benefits-survey/

ii https://www.businessgrouphealth.org/resources/2026-employer-health-care-strategy-survey-executive-summary

iii https://www.ebri.org/docs/default-source/fast-facts-(public)/ff-547-highcost4-23oct25.pdf?sfvrsn=bb5e052f_1

iv https://www.marshmma.com/us/insights/details/health-care-economics.html – :~:text=Specialty drugs–also known%20as,for%20several%20public%20health%20concerns.

v https://www.urban.org/research/publication/48-million-people-will-lose-coverage-2026-if-enhanced-premium-tax-credits

vi https://www.kff.org/health-costs/americans-challenges-with-health-care-costs/

vii https://jamanetwork.com/journals/jamanetworkopen/fullarticle/2842464#google_vignette

viii https://www.patientrightsadvocate.org/2024maristpoll

ix https://www.behaviormodel.org/